As mentioned previously, The Red Garage House is likely to be the first property I hold as a rental. Based on the numbers I’ve put together, I believe that I could likely flip it to a retail buyer if I wanted to, but given that I probably won’t find an excessive number of relatively new properties that will easily cash-flow in my county, when I find them, I will highly consider holding them longer-term.

What I’ll likely do is to rehab it as a rental, and then list it both as a rental and a retail sale. If a buyer (or investor) comes along and is willing to pay our asking price, we’ll flip it; otherwise, once a renter comes along, we’ll rent it and hold onto it.

Here is the quick financial analysis both as a flip and as a rental, assuming it takes three months before I find either a buyer or a tenant…

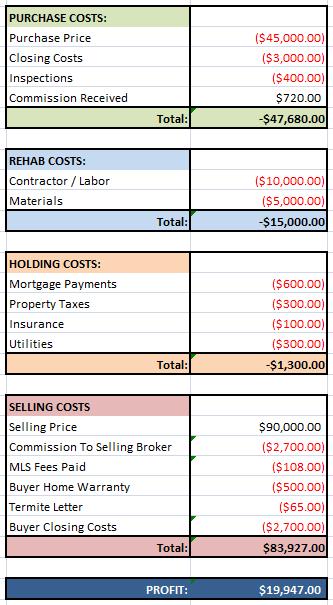

Financial Analysis of Flip

If we were to flip this house, we’d likely list it at $100,000, and be willing to sell it at $90,000 (and pay buyer’s closing costs) for a quick sale. While not much has sold in this neighborhood — and there are three foreclosures on the same block — I haven’t seen any move-in-ready houses for sale at $90K in this area, so that might be enough to attract some buyers.

Given that, here’s the likely profit with a $90K sale:

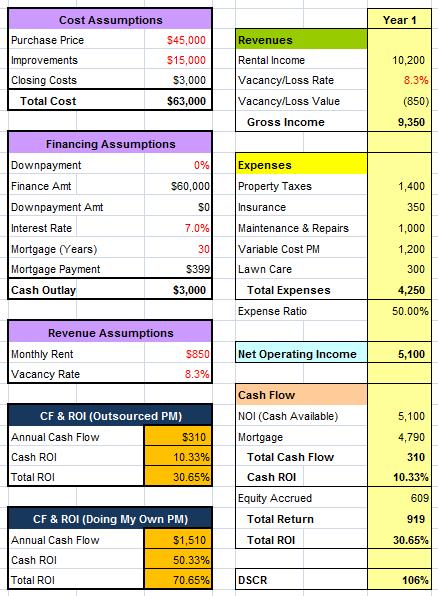

Financial Analysis of Rental

For my rental analysis, I will assume an eventual refinance into a 30-year fixed mortgage, pulling all my invested cash out. I’ll further assume rental rate of $850 (which is $50 less than asking for anything else on that block) and will assume an expense ratio of 50% (using the 50% rule).

Given that, here’s the likely ROI on this rental:

Results

Both results above are very reasonable; as a flip, my profit should approach $20,000. As a rental, my ROI should be over 50% if I property manage it myself (which I will at first), and would still be over 10% if I hired out the property management to a third-party. Most impressive about the rental scenario is that I’d be able to get almost all my cash out at refinancing, and still see positive cash flow under realistic worst-case circumstances.

Given all that, I think I have two reasonable exit strategies — flip or rent — and can decide at a later date which one to pursue…

Interesting calculation. Looks like a pretty solid deal. Typically, for a rental deal, you would do less of a rehab as you don’t want to fix things for a retail buyer.

Steve –

The goal is to get the property into move-in-ready condition, either for a buyer or a renter. In this case, the rehab work would be exactly the same; as a retail sale, it would be the very bottom of the pricing ladder, so the buyer isn’t going to expect any upgrades.

That said, if we sell it, we can negotiate in extras, like washer/dryer, fresh paint on the exterior, etc.

I like that one as a rental also. Anything you can net $5k or more on per year is usually worth your while.

I hate that you have to refi it though, because that’s just money coming right off your bottom line. Wish you could get a 30 yr fixed for it right out of the gate if you plan to keep it as a rental.

Cheers,

– Hakrjak

Hak –

Agreed that it would be nice to save the dual set of closing costs. The one advantage of refi’ing in 6 months is that I can then roll the $15K in rehab costs into the loan, and basically be free-rolling on the property (have none of my own cash invested). AND I’d still be cashflowing!

That, and the fact that I don’t have anyone right now to partner with that can get a conventional loan. In a couple months that problem will hopefully go away.

I agree with Steve, in that it’s rare you would do the same rehab for renting as you would for selling.

How did you calculate your cash ROI?

In this case, the rehab for renting would be the same as a rehab for selling. The goal is to get the property into rental shape, and then try to sell it to an owner-occupant in that condition.

Given that there are many buyers looking for move-in-ready houses in this price range (even in minimal move-in condition), I think there’s a reasonable shot of selling it before we rent it.

As for how I determine cash-on-cash return, the formula is:

COC = Cash Flow / Investment

In this case, as the numbers indicate, my annual cash flow is $310, and my total investment (after I refi out all costs) would be my refi closing costs of $3000.