We closed on the sale of The Poor House today…you can see the detailed schedule and financial results below…

For a large rehab, this project was pretty textbook; we completely replaced the exterior (new roof, gutters, siding, trim, soffit, fascia, decks, etc), remediated a good bit of mold, waterproofed the foundation, finished the basement, and did a full cosmetic rehab on the rest of the interior — all in about 7 weeks. Had we not gotten so much rain at the beginning of the project, it likely would have been finished in under 6 weeks, which is pretty amazing for a gut rehab like this.

I don’t think I ever nailed down a specific budget on this one here on the blog (other than saying “between $45-55K”), but we came in right about where I expected after adding a few upgrades (large front and back decks, basement closet, new windows) that I hadn’t planned. In total, we spent just over $53K, with $45K going to labor and $8K going to materials.

As I’ve mentioned before, I’m thrilled with how this house turned out. It’s not surprising that we received a quick full-price offer after we put it on the market, and it’s not surprising that we received another near-full-price offer shortly after the first contract fell through. This second buyer (and agent) was a pleasure to work with, as the entire process went smoothly and stayed on track from beginning to end.

We almost had some appraisal issues down the stretch, but the mortgage broker did her job well, and we closed on schedule. Here are more detailed breakdowns of our final schedules and financial results…

Timelines

The total holding time on this house was 172 days. It would have been exactly 100 days had the original contract gone through, but considering we essentially completed two separate sales, I guess this isn’t too bad (okay, perhaps I’m rationalizing a bit :)).

Here are the key timeline milestones:

- Purchase Offer Date: 8/25/2009

- Purchase Closing Date: 9/24/2009

- Rehab Completion Date: 11/18/2009

- Sale Listing Date: 11/23/2009

- First Sale Contract Date: 12/8/2009

- Final Sale Contract Date: 2/15/2010

- Sale Closing Date: 3/15/2010

The final contract closed in exactly 4 weeks, which isn’t too bad given it was an FHA buyer.

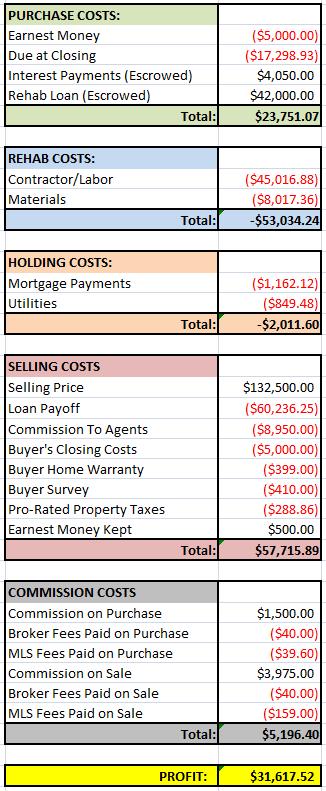

Financials

This was a pretty textbook rehab for us in terms of financial forecasts and results. We were right on track with our projected budget, and our sale price was right about where we expected it to be. At the beginning of the project, I was expecting a $30K profit if everything went as planned, and we exceeded that by just a bit.

Here is the breakdown of financials for this project:

There will be a few more small transactions before the numbers are finalized — insurance overpayment refund, final utility bills, etc — but I expect that we’ll be within $100 one way or the other of this final profit amount.

Our ROI on this project was 105% (we invested just under $30K of our own cash in the deal), and our annualized ROI was about 224%. Not bad, even considering our relatively long hold-time.

Final Statistics

Here are just some of the final statistics that I’ve been tracking for all my projects, and that summarize the success/failure of each project pretty well:

- From Offer to Purchase Time: 30 Days

- Rehab Time: 54 Days

- Selling Days on Market: 84 Days

- Selling Close Time: 28 Days

- Total Hold Time (Close to Close): 172 Days

- Total Profit: $31,617.52

- Return on Investment (ROI): 105.83%

- Annualized ROI: 224.59%

Congrats, J, and nice summary.

Just curious…do you allocate any fixed overhead for your labor calculations (for you, office, etc)?

UJ

Hey UJ,

If I understand your question correctly…

We don’t allocate fixed labor costs to specific projects for Carol and myself. First, it’s difficult to keep track of time spent on specific projects, and more importantly, we attempt to spend as much time as possible working on tasks that will allow us to scale the business in general. So, while we may spend calculable time periods on buying and selling houses, most of the time is spent on more general tasks — such as working with potential lenders, creating marketing collateral, trying to systematize repetitive tasks, etc.

From an accounting standpoint, as far as I know, it really doesn’t make a difference whether we consider ourselves to be an “expense” or whether we consider ourselves to be part of COGS, so we go with the easier method of just treating everything (our salaries, our office, other overhead) as general business expenses. Our accountant hasn’t yelled at us yet (at least not about that :))…

Does that answer your question?

[…] our news sources but please leave us a comment. Click Here! Share blog comments powered by Disqus var disqus_url = […]

Yep, thanks. I was trying to relate your experience to the corporate world, where corporate overhead is sometimes allocated to the business divisions. I think this is sometimes done informally to get a different view of division profitability, not as a legal accounting protocol. But, in a small business, there isn’t much fixed overhead to begin with, and projects are variable.

Guess this would be more of a consideration if you expanded the business into construction, staging, etc…assuming it’s done under one umbrella. But, hey, I’m no accountant…just wondering how you calculated your profits.

Regardless, this project seems a nice success.

UJ

Nice job on this. Can you explain what kind of financing you used? Looks like you had a separate rehab loan? Thanks.

UJ,

I managed P&Ls for many years, and for some reason it was much easier in the corporate world where everyone worked 40 hours/week (or were at least allocated for that period of time), and never spent more their time on more than 1 or 2 major projects simultaneously. Since you mentioned it last night, I’ve been thinking about how to allocate our labor costs across projects, but there’s just no easy way (that would still be meaningful).

Certainly once we start working on other parts of the business as much as we do the house flipping, we’ll have to do this, as we’ll want to get an idea of how profitable each business area is.

But, for now, our scientific method for examining our profitability is that once or twice per year we pay ourselves salary/dividends based on our earnings, and then we look at each other and either say, “Wow, that’s good money for the amount of work we did,” or “Ugh. I can’t believe we worked so hard for THAT!” 🙂

Okay, not quite THAT rudimentary, but close…

Hey Mike –

The loan on this property was a rehab loan, where the bank financed the purchase price + the rehab at 80% LTV.

To break down the numbers a bit more (to give you a better understanding):

– The purchase price on the property was $33K and we asked for $42K in rehab financing. So, the total value of the property (from the perspective of the bank) was $75K.

– The bank will loan 80% of that, or $60K. The other $15K came out of our pockets.

– In total (between earnest money and at the purchase closing), we paid the $15K towards the purchase, $3248.93 towards closing costs and financing fees (a bit higher than usual for various reasons), plus $4050, which goes into an escrow account to be used to pay my interest only mortgage payments for the first year (this is a lender requirements). So, the total we paid was $15,000.00 + $3248.93 + $4050.00 = $22,298.93, which is the aggregate of the first two lines under Purchase Costs.

– In return for paying $22,298.93, we received the property, a loan balance of $60,000 (paid off under Selling Costs), $42K in rehab costs, and $4050 towards our first year’s mortgage payments. The rehab costs and the mortgage payments were both escrowed, and show up on the second two lines under Purchase Costs.

Does that make sense? Sorry if I made it more confusing than it needed to be… 🙂

J, by any measure, you’re doing better than I at this point! And, my one attempt at a small business venture never yielded a paycheck! You and your partner(s) have a lot to be proud about. Truly.

Aside from your own labor, I also wondered about other broad based expenses, e.g., marketing, office space, etc. But, seems you are lean in those areas…marketing mostly word of mouth, I guess, at this point.

…oh, and legal fees.

UJ,

Yup, currently those expenses are a small percentage of our overall income, so their just treated as overhead. For example, we have a home office, so while we can deduct a percentage of mortgage, utilities, Internet fees, etc, it’s still relatively small. Last year, our biggest overhead expenses were accounting and home office equipment (laser printer, for example), but those still were small compared to income.

This year, we will be doing a bunch of marketing for the staging business, and there will be a lot more overhead in that business just because of the furniture purchases, so we’ll be allocating staging costs to that part of the business and actually getting more serious about our accounting, including thinking in terms of multiple P&Ls…

Hello J,

Would you say that the main reasons you were able to get this house for $30,000 was because you paid cash and because of the mold? Also, do you disclose to buyers that there was mold, even though you have completely gotten rid of it? If so, does it seem to be a problem turning some buyers off?

Thanks!!!

Karen

Hey Karen –

First, yes, we always disclose mold to our buyers. On the standard Georgia “Sellers Disclosure Statement” there is a Yes/No question to the effect of, “Were there any water or dampness problems in the basement and/or were any repairs made to fix water or moisture issues?” We answer “Yes” to this question, and then in the additional comments section we say that there was water issues and mold problems when we bought it, and that both waterproofing and mold remediation were completed (and I mention any warranties that may be in effect).

I’ve never had a buyer have an issue with the mold, but we never discourage our buyers from having an independent mold test done to confirm the remediation (we’d even pay for it if a buyer requested it). No-one has ever done it.

As for this property, the $33K purchase was due to a couple reasons:

1. The listing agent was apparently new to listing REO properties, and considered this property to be in horrible shape. She said it had a lot of mold (which was true) and was in “very poor” condition in the listing (hence the name “Poor House”), and I have a feeling that drove many buyers away. The truth was, the house was only a little worse than most REOs we look at, but the scary sounding listing probably kept people away.

2. We know this neighborhood well (we rehabbed “The DIY House” in this subdivision), and went to look at it the very first day it was on the market. We had an offer in that night. I don’t think there were any other offers for the next couple days, by which time ours was already accepted.

So, the bad job by the listing agent, and the fast movement on our part were the two key reasons we got it so cheap.

Sounds good! I look forward to making lots of these types of deals in the future!!

Dude, I am in the wrong part of town 🙁

I found an REO that says “total renovation…investors only..” on the MLS description. Bank is asking $58k, I offer $30k cash (having seen the house) and they counter back at $57k!!!

So if you got this for $30 good for you. I betcha that was Carol working her charm 🙂

I saw this house in person when it was finished and was blown away by the great job you guys did, not surprised at all that you got a full price offer. Congrats!

Thanks, I enjoyed the detailed breakdown of the financials on the deal. The renovation budget did catch my eye–45k in labor, and 8k in materials. Is that the normal balance for your jobs? Or are the materials so much lower becase the labor also represents materials your subs provided? On most of my flips, the balance between labor and materials is usually much closer, so I’m curious!

Hey Greg –

This is actually a pretty typical breakdown between labor and materials on our projects…though that said, I may count “materials” differently than you do…

Our contractors provide all building materials for the job, including siding, roofing materials, paint, lumber, sheetrock, nails, etc, so those costs are counted as part of our Labor costs.

We provide all the finishing materials, including flooring, lighting, plumbing fixtures, appliances, doors, windows, etc. Additionally, there are some things that I account for in a seemingly weird way (for example, we count cabinets and countertops as part of labor and dumpsters as part of materials).

Here is a breakdown of material costs on this project, based on my accounting method:

– Appliances: $2100

– Dumpsters: $945

– Interior Doors: $437

– French Door: $477

– Exterior Doors: $394

– Carpet/Vinyl: $1516

– Bushes: $124

– Lighting Fixtures: $518

– Plumbing Fixtures: $782

– Miscellaneous (Registers, Knobs, Outlets, Switches, Smoke Detectors, etc): $724

If you were to include cabinets and countertops in materials (including the built-in installation charges), that would add another $4275.

So, the finishing materials on this probably were probably somewhere around $12,300…

Makes sense–thanks for the explanation of how you account for materials.